Robot orders accelerate in Q3 as automation becomes strategic initiative

North American robot orders climbed in the third quarter of 2025, signaling renewed momentum in manufacturing automation. According to the latest data released by the Association for Advancing Automation (A3), 8,806 robots valued at $574 million were ordered in Q3, an 11.6% increase in units and 17.2% rise in revenue compared to the same period last year.

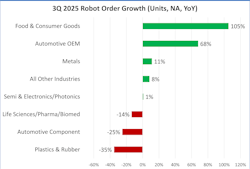

Automotive OEMs and consumer goods drive gains

Key growth sectors in Q3 included food and consumer goods, which jumped 105% year-over-year, and automotive OEMs, which rose 68%. Additional gains came from metals (+11%) and all other industries (+8%), contributing to broad-based improvement across the quarter. In contrast, automotive component orders declined 25%, and plastics and rubber fell 35%, reflecting sector specific capital slowdowns.

Collaborative robots expand market presence

A3 began officially reporting collaborative robot volumes earlier this year. In Q3 2025, companies ordered 1,174 collaborative robots valued at $42 million, accounting for 13.3% of total units and 7.2% of total revenue.

Across the first nine months of 2025, collaborative robot orders reached 4,259 units valued at $156 million, representing 16.1% of units and 9.4% of total revenue. A3 plans to expand future reporting on collaborative robots to include growth rates and sector-specific trends.

Q3 performance lifts year-to-date totals

From January through September 2025, companies in North America ordered 26,441 robots valued at $1.7 billion. These volumes represent a 6.6% increase in units and a 10.6% increase in revenue compared to the same period in 2024.

Non-automotive orders maintain strong momentum

The non-automotive sector continued to lead the robotics market in Q3 2025, accounting for 59% of all robots ordered, according to the latest data. This majority share reflects accelerating momentum across key industries outside of automotive, including food and consumer goods, metals and general manufacturing. These gains highlight a broader shift as manufacturers across diverse sectors turn to automation to enhance productivity as well as address labor shortages, reshoring pressures, and changing customer demands.

“It’s encouraging to see robotics demand improve over last year, with more automation projects steadily returning to the pipeline,” said Alex Shikany, executive vice president at A3. “The market has experienced a substantial amount of economic and policy uncertainty this year, and it’s been a challenging environment for capital investment, but there is upside. We’re seeing sustained interest from companies across the region, with attendance rising at events like Automate, and more leaders are exploring automation as a long-term strategy to strengthen their operations. That enthusiasm is now starting to show up in the order data, particularly across general industry sectors. As industrial production improves into 2026 and supply chains stabilize, we expect automation to remain a strategic priority for manufacturers looking to compete, build resilience and address persistent workforce pressures.”